The Hidden Complexity of Digital Banking

When people envision a digital bank, they typically picture the sleek mobile app, the seamless account opening, and the instant payment confirmations. This is the customer-facing veneer. But beneath this polished surface lies a labyrinth of intricate operations that are critical for any digital banking product to function reliably and scale effectively. Without a robust internal infrastructure, even the most intuitive fintech app buckles under operational strain.

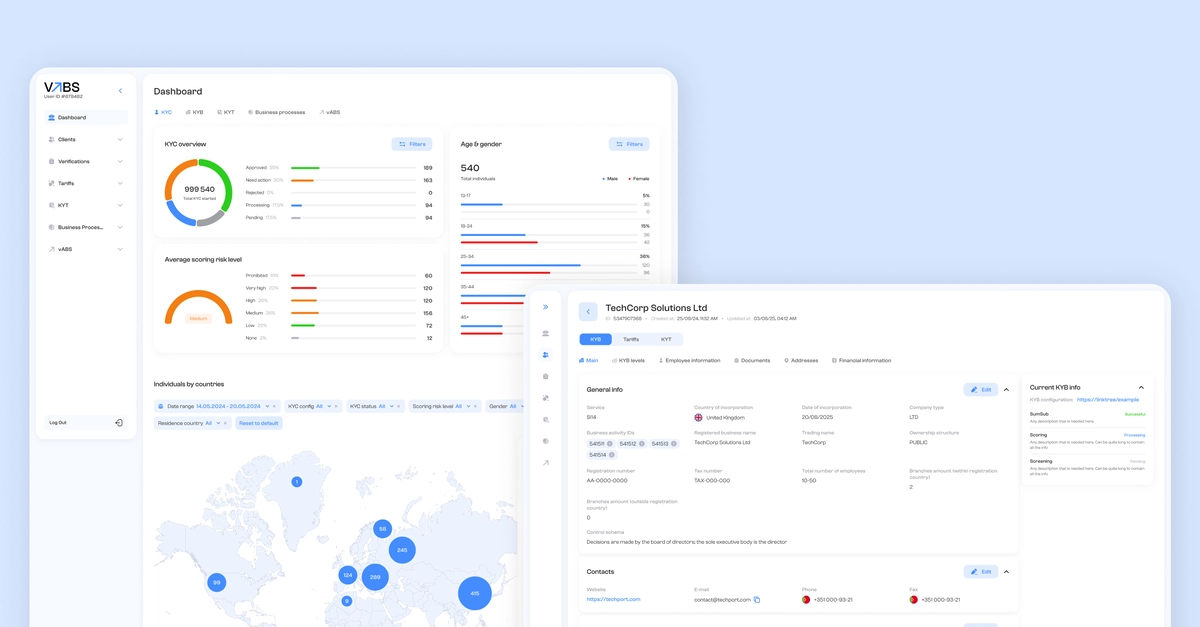

Consider the essential components: a core ledger that accurately tracks every financial movement, sophisticated account logic to handle diverse product types, intelligent payment routing to ensure efficiency and compliance, rigorous transaction monitoring for fraud and anomaly detection, and comprehensive Know Your Customer (KYC) and Know Your Business (KYB) workflows. Add to this Anti-Money Laundering (AML) controls, automated reconciliation processes, complex tariff and limit management, internal approval mechanisms, detailed audit logs, essential support tools, and operational dashboards. This is the unseen engine room.

The absence of this internal layer forces manual interventions, slows down compliance, and creates data silos. Finance teams resort to spreadsheets for reconciliation, support agents lack a holistic client view, and launching new products or integrating new payment providers becomes a bespoke, time-consuming engineering effort. This is precisely the problem that VABS was designed to address.

VABS: A Solution for Operational Scale

VABS, a digital banking back-office solution, emerged from the necessity to streamline these complex internal processes. It acts as the foundational layer that enables digital banks and fintechs to operate efficiently, securely, and compliantly, even as they grow. The design philosophy behind VABS is rooted in understanding that scalability in digital banking is not just about handling more users, but about managing an exponentially increasing volume and complexity of internal operations.

The core of VABS addresses the ledger and account logic. This isn't merely a database; it's a system designed to maintain the integrity and accuracy of financial data under high load, supporting multiple account types, currencies, and product structures. This foundational element is crucial for everything that follows, from transaction processing to regulatory reporting.

Key Components and Functionalities

VABS integrates several critical functionalities that are often managed separately or manually in less mature systems:

- Payment Routing and Monitoring: Efficiently directs payments through appropriate channels while continuously monitoring for suspicious activity. This involves complex logic to select the best route based on cost, speed, and compliance requirements.

- KYC/KYB and AML: Automates and manages the rigorous identity verification and compliance checks required for onboarding customers and monitoring transactions, significantly reducing manual effort and compliance risk.

- Reconciliation: Provides automated tools to match internal records with external statements from payment networks and correspondent banks, a task that is notoriously prone to errors and delays when done manually.

- Tariffs, Limits, and Approvals: Allows for granular configuration of service fees, transaction limits, and internal approval workflows, ensuring business rules are enforced consistently.

- Audit Trails and Reporting: Maintains comprehensive logs of all system activities and user actions, providing essential data for audits, compliance, and business intelligence. Operational dashboards offer real-time insights into system health and key performance indicators.

The surprising detail here is not the existence of these functions, but how VABS aims to integrate them into a cohesive, scalable system. Many platforms offer pieces of this puzzle, but VABS appears to focus on the holistic operational architecture required for a true digital bank.

Lessons Learned in Design and Implementation

Designing a system like VABS involves confronting several challenging realities:

- Data Integrity is Paramount: The core ledger must be immutable and auditable. Any compromise here has cascading financial and regulatory consequences.

- Flexibility for Future Products: The system must be adaptable. Banks constantly innovate, adding new products and services. The back office needs to support this without requiring a complete re-architecture. Think of it less like a rigid filing cabinet and more like a modular workshop that can be reconfigured for different projects.

- Operational Efficiency Drives Profitability: Manual processes are expensive and error-prone. Automation is not a luxury but a necessity for profitability and customer satisfaction in a competitive digital banking landscape.

- Security and Compliance by Design: These are not afterthoughts. They must be embedded into the architecture from the ground up, influencing every decision from data storage to transaction processing.

The challenge for VABS, and indeed any similar platform, is to abstract away the complexity without sacrificing the control and granularity that financial institutions require. It must provide powerful automation while remaining transparent and auditable.

The Impact on Fintech and Digital Banking

For startups and established institutions looking to launch or enhance digital banking services, a well-designed back office is the bedrock of success. VABS represents a move towards more standardized, robust operational frameworks. It allows product teams to focus on user experience and innovation, knowing that the underlying infrastructure can handle the operational load securely and compliantly.

The success of VABS will likely depend on its ability to integrate with existing financial ecosystems, offer clear migration paths for legacy systems, and provide the necessary flexibility for diverse business models. If it can deliver on its promise, it could significantly lower the barrier to entry for new digital banks and enable existing ones to scale more rapidly and profitably.

What nobody has addressed yet is how VABS, or similar platforms, will impact the talent pool required to manage these sophisticated digital back offices. Will it democratize operations, or require a new breed of highly specialized engineers?