The Peril of Shifting Economic Landscapes

Econometric models are the bedrock of economic forecasting, providing frameworks to understand complex relationships between variables and predict future trends. However, these models often operate under the implicit assumption that the underlying economic structures remain constant over time. This assumption, while convenient, is frequently violated. Economic systems are dynamic, influenced by policy changes, technological advancements, global events, and shifts in consumer behavior. When these underlying structures change, models that do not account for such shifts become unreliable, leading to flawed predictions and potentially costly decisions.

The challenge lies in identifying *when* and *how* these structural breaks occur. A model that performed admirably yesterday might be fundamentally misrepresenting today's economic reality. This is particularly critical in time series forecasting, where historical patterns are extrapolated into the future. Without a mechanism to detect and adapt to structural changes, forecasts can degrade rapidly, rendering them useless. The core idea is that the relationships between variables in an economic model are not static; they evolve. Recognizing and quantifying this evolution is paramount for building robust and trustworthy forecasting tools.

Introducing a Framework for Structural Stability Measurement

A recent analysis from Towards Data Science highlights the critical need for a systematic approach to measuring the structural stability of econometric models. The proposed framework emphasizes that simply fitting a model to historical data and assuming its validity for future predictions is insufficient. Instead, it advocates for continuous monitoring and testing of the model's underlying assumptions and relationships.

At its heart, structural stability refers to the invariance of the model's parameters and the functional relationships between variables over time. When these parameters or relationships drift or change abruptly, a structural break has occurred. These breaks can manifest in various ways: a sudden shift in the intercept, a change in the slope of a regression line, or a complete alteration of the functional form of the relationship between variables. Detecting these shifts is akin to a doctor monitoring a patient's vital signs; any deviation from the norm signals a potential issue that requires attention.

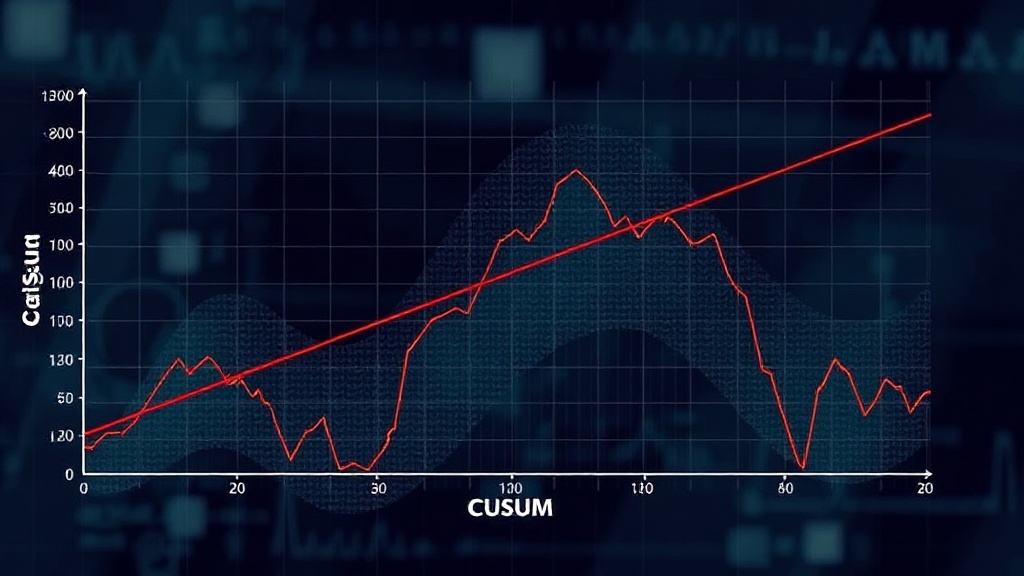

The proposed methodology involves a series of statistical tests designed to detect these changes. These tests can be broadly categorized into two types: tests for parameter stability and tests for functional form stability. Parameter stability tests, such as the CUSUM (Cumulative Sum) test or the Chow test, examine whether the estimated coefficients of the model remain constant over different sub-samples of the data. Functional form stability tests, on the other hand, assess whether the overall structure of the model, including non-linearities and interactions, holds true across different time periods.

The simplicity of the core idea belies its profound importance. For any time series forecasting task, understanding that the past is not always a perfect predictor of the future is the first step. The next, more challenging step is to quantify this uncertainty. This framework provides a structured way to do just that. It moves beyond merely fitting a line through data points to actively questioning whether that line still accurately represents the underlying economic forces at play.

Implications for Forecasting and Decision Making

The implications of failing to account for structural stability are far-reaching. In macroeconomics, models used for policy simulation might suggest interventions that are ineffective or even counterproductive if the economic structure has shifted. For financial institutions, models predicting asset prices or credit risk can lead to substantial losses if they do not adapt to changing market dynamics. Even in microeconomics, models of consumer demand can become obsolete if consumer preferences or the competitive landscape evolve.

Consider a model forecasting housing prices. It might be built on data from a period of stable interest rates and steady population growth. If interest rates suddenly spike or a major employer leaves town, the relationships the model learned—how price reacts to inventory, for instance—may no longer hold. Without a stability check, the model would continue to churn out forecasts based on outdated assumptions, potentially misinforming real estate investors or policymakers.

The framework suggests a workflow where models are not just built and deployed, but continuously monitored. This involves setting up automated checks that run periodically, comparing model performance on new data against its historical performance and explicitly testing for parameter and functional form changes. When a significant deviation is detected, it signals that the model needs to be re-evaluated, re-estimated, or even fundamentally redesigned. This iterative process ensures that the models remain relevant and reliable in the face of evolving economic conditions.

This approach transforms econometric modeling from a static exercise into a dynamic, adaptive process. It acknowledges that economic systems are living entities, constantly in flux. By providing tools to measure and react to these changes, the framework aims to enhance the trustworthiness and practical utility of econometric forecasts. It’s about building models that are not just statistically sound on past data, but also resilient to the inevitable uncertainties of the future.

The Unanswered Question: What is the Optimal Frequency for Stability Testing?

While the necessity of measuring structural stability is clear, one critical question remains largely unaddressed: what is the optimal frequency for conducting these stability tests? The choice between daily, weekly, monthly, or quarterly checks depends heavily on the volatility of the economic system being modeled, the specific application, and the computational resources available. A trade-off exists between the cost of frequent testing (computational expense, potential for false alarms) and the risk of using a degraded model for too long. Determining this optimal cadence is a practical challenge that requires further research and empirical validation across diverse economic contexts.